It’s 11:47 PM on a Tuesday in January. You’re staring at a payroll remittance summary that doesn’t balance, and somewhere between the Canada Pension Plan deduction column and the Employment Insurance premium line, the numbers went sideways. You’ve been toggling between the CRA payroll tables and your accounting software for forty minutes.

The T4s are due in weeks. And the knot in your stomach tells you one thing clearly: you never fully understood how these two deductions actually differ.

You’re not alone. CPP and EI are the two most common payroll deductions in Canada — every employer touches them every pay run — yet a surprising number of business owners and bookkeepers confuse their purpose, their contribution structures, and their reporting rules. That confusion doesn’t stay theoretical for long. It surfaces as payroll reporting mismatches, incorrect T4 slips, and eventually, letters from the Canada Revenue Agency that nobody wants to open.

This article breaks the whole thing apart. What CPP actually funds versus what EI covers. Who pays what. How the math works. Where employers consistently make mistakes. And how to build a payroll workflow that keeps you clean with the CRA year after year.

The quick verdict: CPP is a mandatory retirement and disability savings program where employers match employee contributions dollar for dollar. EI is a government-run insurance program providing temporary income support, where employers pay 1.4 times the employee’s premium.

Both hit every payroll cycle, both appear on T4 slips, and both carry real penalties when handled incorrectly — but they serve fundamentally different purposes and follow different calculation rules. Knowing the distinction isn’t optional. It’s the baseline of Canadian payroll compliance.

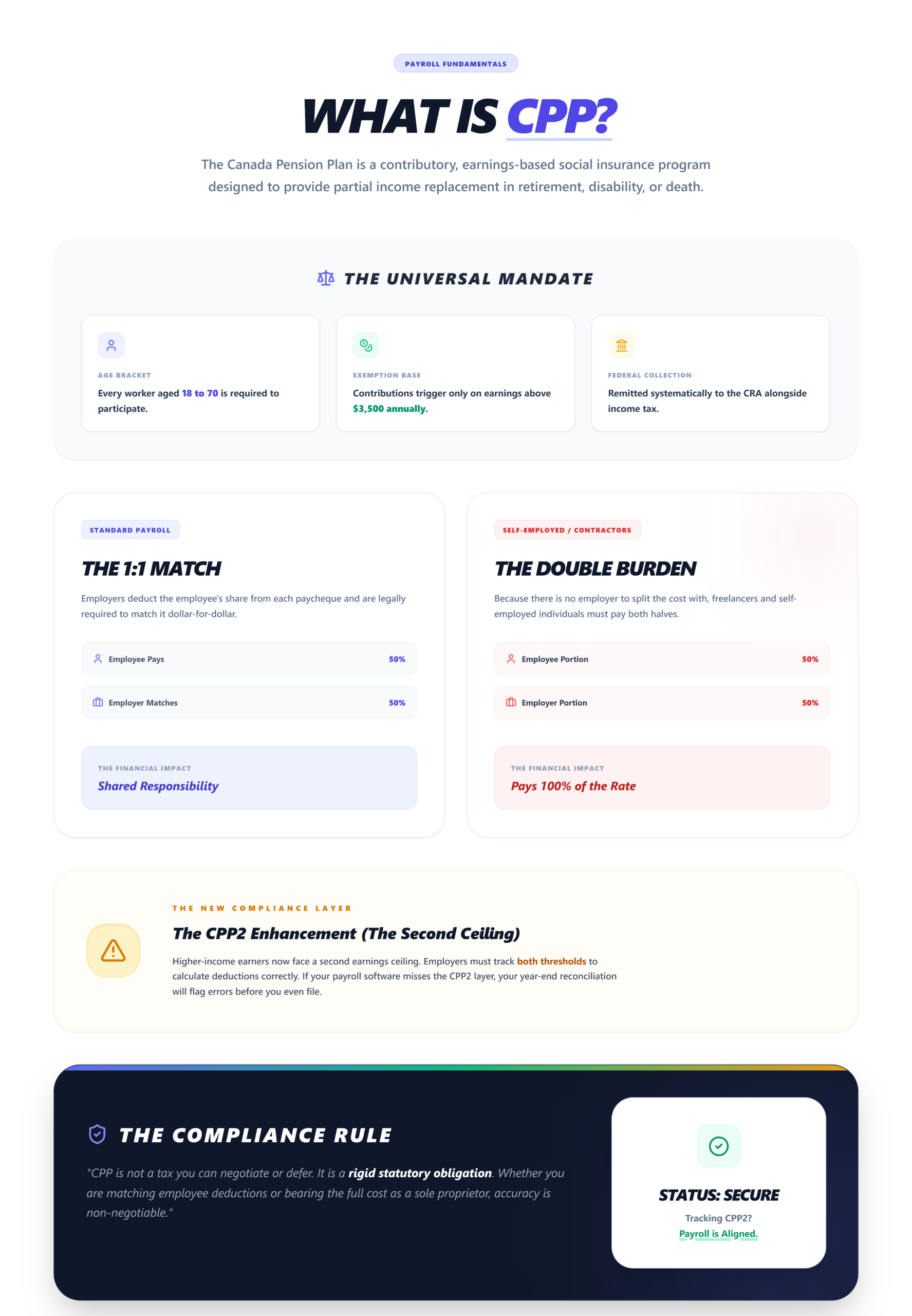

What Is CPP?

The Canada Pension Plan is a contributory, earnings-based social insurance program administered by the federal government. Its primary purpose: provide workers with a partial income replacement in retirement, or upon disability or death.

Every employee aged 18 to 70 who earns above the basic exemption amount (currently $3,500 annually) must contribute to CPP. Employers are required to deduct the employee’s share from each paycheque and remit it alongside their own matching contribution. That’s a critical detail — the employer’s CPP obligation is a true dollar-for-dollar match of what the employee pays.

Self-employed individuals carry a heavier load. Because there’s no employer to split the cost with, self-employed workers pay both the employee and employer portions — effectively doubling their CPP contribution rate. This is calculated on net self-employment income and reported on the annual tax return.

With the introduction of CPP2 (the second additional CPP enhancement), higher-income earners now face a second earnings ceiling. Employers need to track both thresholds to calculate deductions correctly. Miss the CPP2 layer, and your year-end reconciliation will flag errors before you even file.

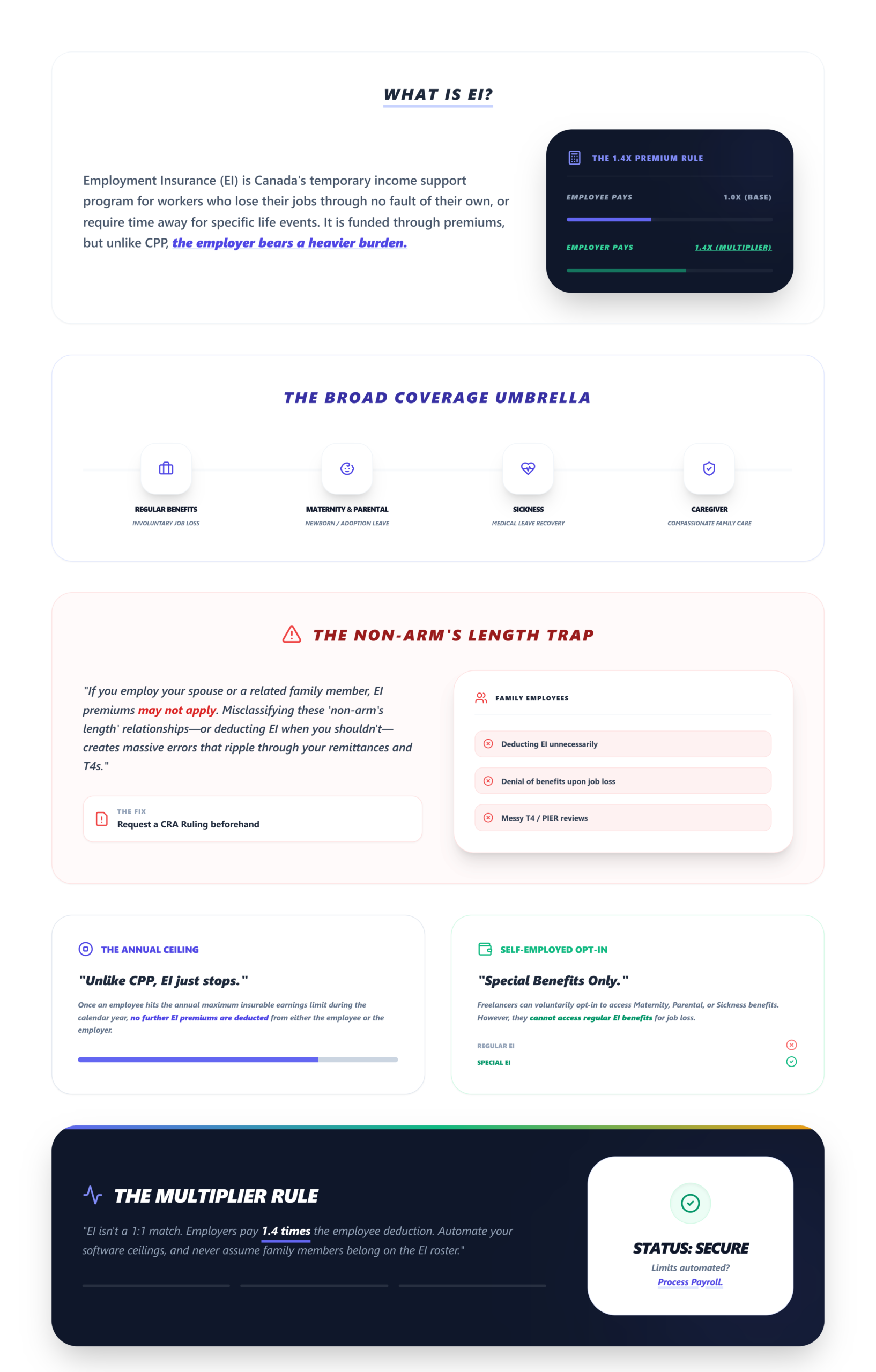

What Is EI?

Employment Insurance is Canada’s federally managed program designed to provide temporary income support to workers who lose their jobs through no fault of their own, or who need time away from work for specific life events.

EI covers a broader range of situations than most employers realize — regular benefits for job loss, yes, but also maternity benefits, parental benefits, sickness benefits, compassionate care, and family caregiver benefits. The program is funded through premiums deducted from employee pay, with the employer contributing a premium that’s 1.4 times the employee’s share.

Unlike CPP, EI premiums stop once the employee reaches the annual maximum insurable earnings. Once that ceiling is hit during the calendar year, no further EI premiums are deducted — from either party.

Here’s a friction point that catches new employers off guard: certain employment relationships are exempt from EI. For example, if you employ your spouse or a related family member in specific circumstances, EI premiums may not apply. Misclassifying these relationships — or failing to apply the exemption — creates errors that ripple through your remittances and T4s.

Self-employed individuals can opt into EI special benefits (maternity, parental, sickness, compassionate care) through the Canada Revenue Agency, but they cannot access regular EI benefits for job loss. This opt-in is voluntary, and once registered, it comes with a minimum participation period.

CPP vs EI: Key Differences

Here’s the side-by-side breakdown every employer should have pinned near their payroll workstation:

- Purpose

CPP: Retirement, disability, and survivor income | EI: Temporary income support (job loss, leave) - Who Contributes

CPP: Employee + Employer | EI: Employee + Employer - Employer Contribution Rule

CPP: Matches employee contribution 1:1 | EI: Pays 1.4× the employee premium - Self-Employed

CPP: Must pay both portions | EI: Voluntary opt-in for special benefits only - Reported On

CPP: T4 slip (Boxes 16 & 17) | EI: T4 slip (Boxes 18 & 24)

The structural difference that matters most operationally: CPP is a 1:1 match. EI is a 1.4× multiplier. Get those ratios wrong, and every remittance you send to the CRA will be off.

Who Pays CPP and EI?

Both programs operate on a shared-cost model, but the split isn’t identical.

CPP: The employee pays a percentage of pensionable earnings (after the $3,500 basic exemption), and the employer matches that amount exactly. For 2024, the employee rate is 5.95% on earnings up to the first ceiling, with an additional CPP2 rate of 4% on earnings between the first and second ceilings. Employer obligations mirror these figures precisely.

EI: The employee pays a premium rate on insurable earnings (1.66% for 2024), and the employer pays 1.4 times that amount — so 2.324% of the same insurable earnings. Some employers with a registered wage-loss replacement plan qualify for a reduced EI premium rate, which changes the multiplier slightly.

Self-employed CPP: Sole proprietors, partners, and independent contractors pay the combined employee-employer share. There’s no matching from anyone else. This is one of the largest non-optional costs of self-employment in Canada.

EI exceptions: Business owners who control more than 40% of voting shares in a corporation are generally not eligible for EI and shouldn’t have premiums deducted. Family employees in non-arm’s-length arrangements may also be exempt depending on the nature of the employment. These edge cases require careful classification — and documentation.

How Employers Calculate CPP and EI Contributions

The math isn’t complicated in isolation. The challenge is doing it correctly across dozens or hundreds of pay periods, with changing employee statuses, mid-year hires, and employees who hit annual maximums at different times.

CPP calculation: Take the employee’s gross pensionable earnings for the pay period, subtract the prorated basic exemption, and multiply by the contribution rate. The employer owes the same dollar amount. For CPP2, apply the second-tier rate on earnings between the first and second ceilings.

EI calculation: Multiply the employee’s insurable earnings for the period by the EI premium rate. The employer owes 1.4 times that result. Stop deducting once the employee’s year-to-date insurable earnings reach the annual maximum.

Most modern payroll software handles these calculations automatically — but “automatically” doesn’t mean “correctly.” If employee records contain wrong birth dates, incorrect employment types, or outdated rate tables, the software will faithfully produce wrong numbers. Verifying deductions against the CRA’s online payroll deductions calculator at least quarterly is a practice that pays for itself at year-end.

Common CPP and EI Mistakes Employers Make

These are the errors that show up during payroll reconciliation workflows and CRA reviews:

- Incorrect exemption handling: Failing to apply the CPP basic exemption, or applying EI exemptions to employees who don’t qualify, throws off every downstream calculation.

- Outdated contribution rates: Using last year’s rates into January — even for one or two pay runs — creates cumulative errors that are painful to correct retroactively.

- Employee classification errors: Treating a contractor as an employee (or vice versa) changes CPP and EI obligations entirely. The CRA’s worker classification rules aren’t suggestions.

- Reconciliation mismatches: When the total CPP and EI remitted during the year doesn’t match the sum of employee T4s, the CRA will notice. These mismatches often stem from mid-year corrections that weren’t carried through to the remittance account.

- T4 reporting errors: Transposing CPP and EI amounts between boxes, or failing to report CPP2 contributions in the correct fields, triggers reassessments and employee complaints during tax season.

Avoiding these payroll mistakes that can trigger CRA penalties starts with clean data entry and ends with disciplined reconciliation before filing.

How CPP and EI Affect T4 Reporting

Every T4 slip issued to an employee must accurately reflect the CPP and EI amounts deducted during the calendar year. Box 16 (Employee’s CPP), Box 17 (Employee’s CPP2), Box 18 (Employee’s EI), and Box 24 (EI insurable earnings) are non-negotiable.

The employer’s share of CPP and EI doesn’t appear on the T4 — it’s reported through the remittance process and reconciled on the PD7A or through the CRA’s payroll account. Getting these boxes right matters beyond compliance. Employees use T4 data to file their personal tax returns. Incorrect CPP or EI figures lead to reassessments, frustrated employees, and amended slips — none of which reflect well on your payroll operation.

Understanding the differences between T4 and T4A slips helps ensure you’re issuing the right form to the right worker in the first place. Year-end reconciliation should compare total CPP and EI deducted across all T4s against total remittances made to the CRA during the year. Any variance needs investigation before filing. This is where solid payroll reconciliation workflows become non-negotiable.

Best Practices for Managing CPP and EI Deductions

Use this as your operational checklist:

- ✅ Update CPP and EI rates, maximums, and exemption amounts every January 1

- ✅ Verify employee birth dates and employment status in your payroll system quarterly

- ✅ Confirm self-employed CPP obligations are calculated at the combined rate

- ✅ Apply EI exemptions only where CRA criteria are clearly met and documented

- ✅ Reconcile CPP and EI remittances against payroll registers monthly

- ✅ Cross-check T4 totals against CRA remittance records before year-end filing

- ✅ Monitor payroll remittance deadlines in Canada to avoid late penalties

Frequently Asked Questions

Is CPP mandatory in Canada?

Yes. CPP contributions are mandatory for all employees aged 18 to 70 who earn above the $3,500 basic exemption. Employees aged 65 to 70 can elect to stop contributing by filing a CPT30 form. Self-employed individuals must also contribute on net self-employment income. There is no opt-out for workers under 65.

Who is exempt from EI?

Employees who own more than 40% of a corporation’s voting shares are generally exempt. Non-arm’s-length employees (such as family members) may also be exempt depending on the employment terms. Certain self-employed individuals are exempt from regular EI premiums unless they voluntarily opt into special benefits through the CRA.

Do employers match CPP and EI?

Employers match CPP contributions at a 1:1 ratio — dollar for dollar with the employee’s deduction. For EI, employers pay 1.4 times the employee’s premium, not a direct match. Both amounts are remitted together to the Canada Revenue Agency on the employer’s regular remittance schedule.

Can self-employed individuals pay EI?

Self-employed individuals can voluntarily register for EI special benefits, which include maternity, parental, sickness, and compassionate care benefits. They cannot access regular EI benefits for loss of income or work. Once registered, there is a waiting period before benefits can be claimed, and premiums must be paid on the annual tax return.

Are CPP and EI reported on a T4?

Yes. Employee CPP contributions appear in Box 16, CPP2 contributions in Box 17, EI premiums in Box 18, and EI insurable earnings in Box 24 of the T4 slip. The employer’s share is not shown on the T4 but is tracked through CRA remittance records and reconciled at year-end.

Master Your Payroll Compliance

Don’t let payroll remittances turn into a year-end crisis. LedgerNext automates your deductions, ensures compliance with CRA rates, and keeps your reporting audit-ready.