A signed contract sits on your desk. It reads “Independent Contractor Agreement” in bold across the top. The worker invoices monthly, sets their own hours, and has their own laptop. Open and shut, right?

Not even close.

Worker classification is one of the most misunderstood areas of payroll compliance in Canada. Businesses assume a contract dictates the relationship. CRA doesn’t care what the contract says—they evaluate the actual working relationship. The title on the agreement is a starting point, not a finish line.

Get it wrong, and you’re staring down retroactive CPP and EI assessments, penalties, interest, and the kind of audit trail that keeps controllers awake at 2 a.m. Get it right, and your payroll obligations, tax reporting, and remittance workflows stay clean.

This guide breaks down exactly how CRA determines worker classification, walks through each evaluation factor with real-world examples, and gives you a practical decision checklist you can use before onboarding your next worker.

Employee vs Contractor in Canada: Quick Answer

- CRA determines worker status based on the actual working relationship, not the contract title.

- Key factors include control over the work, ownership of tools, chance of profit, risk of loss, and integration into the business.

- A worker labeled as an independent contractor may still be classified as an employee by CRA.

- Correct classification directly affects CPP contributions, EI premiums, T4 or T4A reporting, payroll deductions, and remittance obligations.

- Misclassification can trigger reassessments, back taxes, penalties, and interest.

Why Worker Classification Matters

Classification isn’t an HR formality. It determines your entire payroll and tax reporting structure.

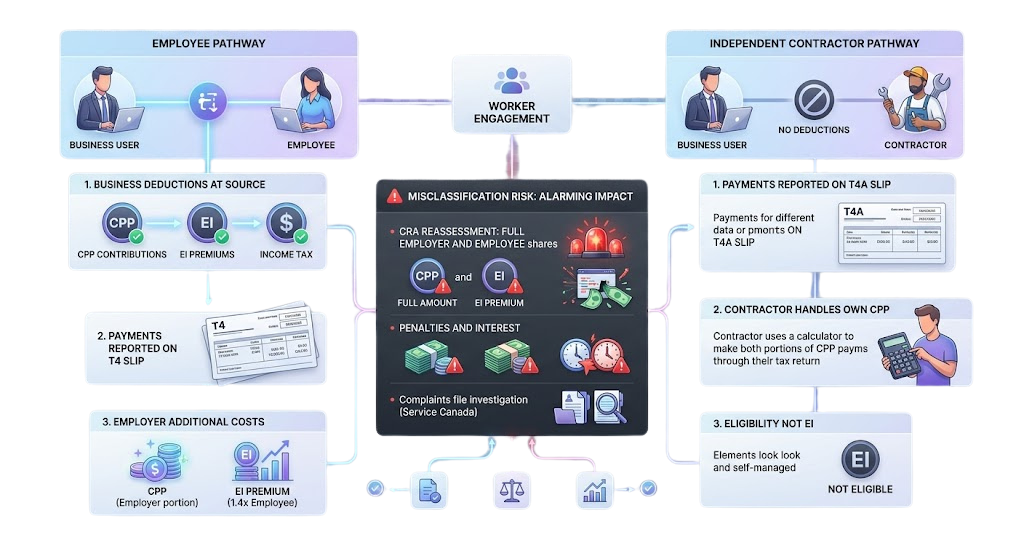

When a worker is classified as an employee, the business must deduct and remit CPP contributions, EI premiums, and income tax at source. These amounts are reported on a T4 slip. The employer also pays the employer portion of CPP and 1.4 times the employee’s EI premium.

When a worker is classified as an independent contractor, none of those deductions apply. The business reports payments on a T4A slip. The contractor handles their own CPP contributions (both portions) through their tax return and is generally not eligible for EI.

Misclassifying an employee as a contractor means those CPP and EI amounts were never deducted or remitted. CRA can reassess the business for the full employer and employee shares, plus penalties and interest. Understanding CPP and EI deduction requirements is non-negotiable for any business engaging workers.

The operational impact extends beyond tax. Misclassified workers may file complaints. Service Canada may investigate EI eligibility. The ripple effects touch payroll, legal, and finance simultaneously.

What Is an Employee?

An employee works under the direction and control of the employer. The employer decides how, when, and where the work gets done.

Typical markers:

- Fixed schedule set by the employer

- Direct supervision of tasks and methods

- Payroll deductions for CPP, EI, and income tax

- T4 reporting at year-end

- Tools, equipment, and workspace provided by the employer

- No opportunity to profit beyond their salary or wages

Example: A bookkeeper works in your office Monday to Friday, uses your accounting software, follows your internal processes, and receives a biweekly paycheque with deductions. That’s an employee—regardless of what their offer letter says.

What Is an Independent Contractor?

A contractor operates as a separate business entity. They control how and when the work is performed, bear their own expenses, and typically serve multiple clients.

Typical markers:

- Autonomy over methods, schedule, and workflow

- Invoices the business for services rendered

- Owns their tools, equipment, and software

- Carries business risk (e.g., liability insurance, unpaid invoices)

- T4A reporting by the payer at year-end

- Opportunity to profit or lose based on their own decisions

Example: A freelance graphic designer works from their home studio, uses their own Adobe suite, invoices three different companies monthly, and sets their own rates. That’s a contractor.

Employee vs Contractor in Canada: Key Differences

Here is the side-by-side comparison:

- Control over work

Employee: Employer directs how, when, where | Contractor: Worker decides methods and schedule - Tools & equipment

Employee: Provided by employer | Contractor: Owned by worker - CPP

Employee: Employer deducts and remits (both shares) | Contractor: Worker pays both shares on tax return - Tax reporting

Employee: T4 slip | Contractor: T4A slip - Business risk

Employee: None—employer absorbs | Contractor: Worker absorbs losses

Understanding the differences between T4 and T4A reporting is critical here. Filing the wrong slip is one of the fastest ways to flag an audit.

How CRA Determines Worker Classification

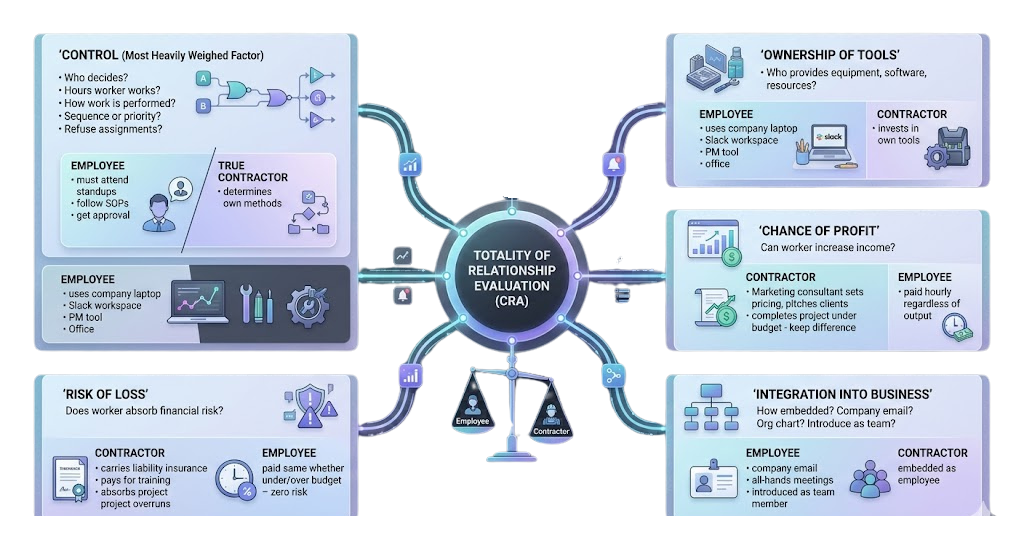

CRA doesn’t rely on a single test. They evaluate the totality of the working relationship across five factors. No single factor is decisive on its own.

Control

This is the factor CRA weighs most heavily. Who decides: What hours the worker works? How the work is performed? The sequence or priority of tasks? Whether the worker can refuse assignments? Example: If your “contractor” must attend daily standups, follow your internal SOPs, and get approval before deviating from a process—that looks like control. CRA sees an employee. A true contractor determines their own methods.

Ownership of Tools

Who provides the equipment, software, and resources needed to complete the work? Example: A contractor who uses your company laptop, your Slack workspace, your project management tool, and your office space isn’t operating independently. CRA will question whether they’re truly running their own business. Contractors typically invest in their own tools.

Chance of Profit

Can the worker increase their income through their own decisions—by working more efficiently, negotiating higher rates, or taking on additional clients? Example: A marketing consultant who sets their own pricing, pitches new clients, and can complete a project under budget (keeping the difference) has a genuine chance of profit. An employee paid $30/hour regardless of output does not.

Risk of Loss

Does the worker absorb financial risk? This includes: Covering their own expenses (travel, materials, insurance), risk of non-payment or bad debts, liability for errors or rework at their own cost. Example: A contractor who carries professional liability insurance, pays for their own training, and absorbs the cost of project overruns is bearing genuine business risk. An employee who gets paid the same whether the project runs over budget or not bears zero financial risk.

Integration Into the Business

How embedded is the worker in daily operations? Do they appear to clients as part of your team? Do they use a company email address? Are they included in org charts? Example: A “contractor” who has a company email, attends all-hands meetings, and is introduced to clients as a team member is deeply integrated. CRA views that as an employment relationship.

Common Worker Classification Mistakes

- Assuming the contract dictates status

CRA looks past the paperwork. If the day-to-day reality doesn’t match the contract, the contract loses. - Issuing T4A slips for workers who function as employees

The slip doesn’t change the relationship. It just creates a paper trail of non-compliance. - Ignoring CRA’s evaluation criteria

Defaulting to “contractor” because it’s cheaper without reviewing the five factors. - Inconsistent treatment

Paying two people doing identical work differently—one as employee, one as contractor. - Undocumented relationships

No written agreement, no scope of work, no invoices. No evidence to show when CRA asks.

Consequences of Misclassification

Misclassification isn’t a grey area for CRA. The consequences are financial and operational: CPP reassessments (employer and employee shares, retroactively), EI reassessments (employee premiums plus the 1.4x employer premium), back taxes, interest compounding from original due dates, and penalties for failure to deduct, remit, or file correctly. Avoiding payroll mistakes that can lead to CRA penalties starts with getting classification right from day one.

Employee vs Contractor Decision Checklist

Before classifying any worker, run through these questions:

- ✅ Who controls how and when the work is performed?

- ✅ Who provides the tools, equipment, and software?

- ✅ Can the worker earn additional profit through their own decisions?

- ✅ Does the worker carry financial risk (expenses, liability, bad debts)?

- ✅ Is the worker integrated into daily business operations?

- ✅ Does the worker serve multiple clients?

- ✅ Does the worker invoice for services?

How Worker Classification Affects Payroll Reporting

Employee classification triggers T4 reporting, CPP deductions, EI deductions, income tax withholding, and regular remittances to CRA. Miss a payroll remittance deadline in Canada and penalties start accruing immediately. Contractor classification triggers T4A reporting with no source deductions. Businesses with a mix of employees and contractors need clean payroll reconciliation workflows to ensure T4s, T4As, remittance amounts, and general ledger entries all tie out at year-end. LedgerNext helps businesses maintain that consistency—connecting payroll data, bookkeeping records, and accounting workflows so nothing falls through the cracks.

Master Your Payroll Compliance

Don’t let payroll remittances turn into a year-end crisis. LedgerNext automates your deductions, ensures compliance with CRA rates, and keeps your reporting audit-ready.

Frequently Asked Questions

Can a contractor receive a T4?

No. T4 slips are issued to employees only. If a worker is reclassified as an employee by CRA, the business must issue amended T4 slips and remit outstanding deductions.

Can an employee receive a T4A?

Generally no. T4A slips report payments to contractors, not employees. Issuing a T4A to someone who functions as an employee does not change their classification.

Does CRA use contracts alone to determine worker status?

No. CRA evaluates the actual working relationship. A contract labeling someone as an independent contractor holds little weight if the day-to-day reality resembles employment.

What happens if a worker is misclassified?

CRA can reassess the business for unpaid CPP, EI, and income tax, plus interest and penalties. The employer may owe both the employer and employee portions retroactively.

Do contractors pay CPP?

Yes. Self-employed contractors pay both the employee and employer portions of CPP through their annual tax return.

Do contractors pay EI?

Generally no. Independent contractors are not required to pay EI unless they opt into the EI program for self-employed individuals for special benefits.

Can worker status change over time?

Yes. A relationship that starts as a genuine contractor arrangement can evolve into employment if control, integration, and other factors shift. Businesses should reassess periodically.

Can a person be both an employee and a contractor?

Yes. A worker can be an employee for one role and a contractor for a completely separate engagement with the same business, provided the contractor role genuinely meets CRA’s criteria.