It’s 11 PM on the last Thursday of the month, and your team is still chasing a $47.32 variance across three client accounts. The transactions were from two weeks ago. The supporting documentation? Somewhere in a client’s email thread, maybe. Or a shoebox. The actual reconciliation—matching, confirming, signing off—would’ve taken minutes if the data had been clean when it arrived.

I’ve watched this pattern repeat across dozens of accounting firms. The reconciliation itself isn’t the hard part. The hours disappear into everything that happens before reconciliation: inconsistent categorization, missing documents, inherited client records that need cleanup before anyone can even start matching.

By the end of this guide, you’ll be able to identify the exact upstream bottlenecks slowing your bank reconciliation and implement the workflow changes that Canadian accounting firms are using to cut their reconciliation time significantly.

What Is Bank Reconciliation (and Why Does It Feel So Broken)?

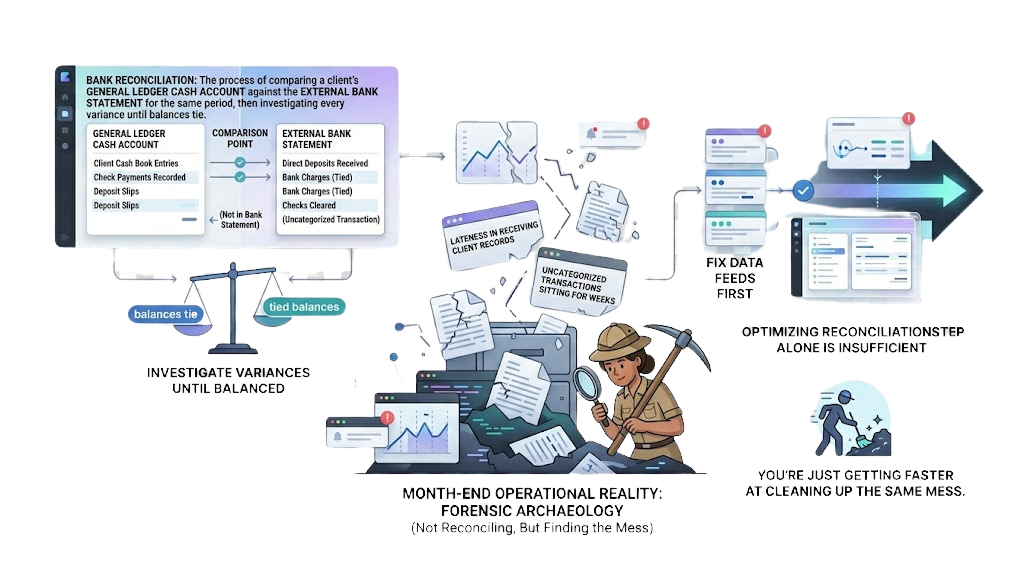

Bank reconciliation is the process of comparing your client’s general ledger cash account against the external bank statement for the same period, then investigating every variance until balances tie. If you want the full breakdown, our complete guide to bank reconciliation covers the mechanics in depth.

But here’s what no textbook tells you: for most accounting teams, the process feels broken not because reconciliation is conceptually difficult, but because the data feeding into it is messy.

Client records arrive late. Transactions sit uncategorized for weeks. And by the time month-end hits, your team isn’t reconciling—they’re doing forensic archaeology.

That distinction matters. Because if you keep optimizing the reconciliation step without fixing what feeds into it, you’re just getting faster at cleaning up the same mess.

Pre-Flight Check: Are You Actually Ready to Speed This Up?

Before changing anything in your bookkeeping workflows, you need honest answers to a few things. Your Stop/Go test: Can you describe, in one sentence, where your reconciliation time actually goes each month? If the answer is “matching transactions,” you might just need better software. But if it’s “figuring out what half these transactions even are,” the fix is upstream.

Here’s what you need locked down first:

- Bank feed connectivity. If your bank feed is stale or disconnected, automated matching can’t help you. Confirm feeds are pulling daily.

- A standardized chart of accounts across similar client portfolios. If every client has a different structure, your team is re-learning categorization logic every time they switch files.

- Clear ownership. Someone on the accounting team needs to own reconciliation cadence—not just execution, but the follow-up on outstanding items.

- Client cooperation. If clients send records in batches once a month instead of keeping things current, your reconciliation will always start with a data cleanup phase.

If any of these are missing, fix them first. Everything below assumes they’re in place.

Phase 1: Fix Transaction Categorization Before It Reaches Reconciliation

Inconsistent transaction categorization is the single biggest reason reconciliation takes longer than it should.

What firms experience: Accounting teams spend hours reviewing transactions that should have been categorized correctly the first time. One team member codes a bank fee to “Office Expenses.” Another codes the identical charge to “Bank Charges”. Descriptions vary across banks—TD formats things differently than RBC, and both differ from credit union exports. Why it happens: Rules are inconsistent. There’s no centralized categorization logic. And when you’re managing dozens of client portfolios, the problem compounds fast.

The business impact: Review work increases. Reconciliation exceptions multiply. Client reporting becomes less reliable because the financial records feeding those reports were categorized differently depending on who touched them.

What to do: Build standardized categorization rules per client type and enforce them through your software, not through tribal knowledge. If your platform supports rule-based transaction categorization for accurate bookkeeping, set those rules once and let them apply automatically. Review exceptions only—not every line.

Visual checkpoint: When this phase is working, your transaction list should show the vast majority of entries already categorized, with only a short exception queue requiring manual review. If you’re still eyeballing every line, the rules aren’t working.

Phase 2: Stop Letting Duplicate and Ghost Entries Pile Up

Duplicate entries are sneaky. They don’t always show up as obvious errors—sometimes two entries net out against each other, and the cash balance looks correct, but the underlying detail can’t withstand audit scrutiny.

What firms experience: A client’s payroll run posts twice. A transfer between accounts gets recorded on both sides but with slightly different dates. The variance is zero, so nobody investigates—until audit season. Why it happens: Manual data entry. Bank feeds that occasionally double-import. And the human tendency to move on when the balance ties.

The fix: Force every discrepancy into a categorized reconciling-item list. Don’t just clear items because the net effect is zero.

Phase 3: Break the Month-End Bottleneck

Month-end reconciliation often becomes the single biggest bottleneck in accounting firm operations because unresolved issues accumulate throughout the month.

What firms experience: The first three weeks of the month feel manageable. Then week four hits, and suddenly every client account needs attention simultaneously. The accounting team scrambles. Deadlines slip. Financial statement preparation gets delayed.

Root cause: Firms treat reconciliation as a monthly event instead of a continuous process. When you reconcile only at month-end, you’re stacking 30 days of timing differences, uncategorized transactions, and missing documentation into a single window. The sources are clear on this: delaying reconciliation makes discrepancies pile up and become harder to resolve. High-transaction accounts may need weekly or even daily attention.

What to do: Shift to rolling reconciliation. Even reconciling weekly for your highest-volume clients dramatically reduces the month-end crunch. Use a month-end close checklist for Canadian accounting firms to standardize what gets done and when—so nothing slides into that final week.

Phase 4: Automate the Repetitive Matching

Manual reconciliation becomes impractical as transaction volume grows. That’s not an opinion—it’s math. As client portfolios expand, reconciliation workloads increase much faster than headcount.

What firms experience: A firm managing 30 clients can probably handle manual matching. At 80 clients, the same team is drowning. Not because the work got harder, but because the volume of routine matches overwhelmed the manual process.

What to do: Automated matching should handle the routine deposits, payments, and transfers. Your team’s time should go toward exception items—the transactions that actually need human judgment.

Where LedgerNext Fits

Spending Too Much Time on Data Cleanup Before Reconciliation Even Starts?

We built LedgerNext specifically for Canadian accounting firms dealing with this exact problem. The platform converts raw bank statements into categorized, tax-ready financial data using rule-based categorization and automated transaction matching—so your team works exception items, not every line. If your reconciliation bottleneck starts before reconciliation, request a demo and see how the upstream cleanup disappears.

The “Ugly Truth”: Where Reconciliation Actually Breaks Down

- Reconciliation never reaches zero

Problem: Old outstanding items rolling forward month after month.

Fix: Rebuild the rec from the bank statement date forward instead of patching an inherited schedule. - Bank feed matches are mostly right, but a few lines never auto-match

Problem: Naming, date, or amount formatting differences across banks.

Fix: Create a manual exception queue; normalize descriptions before matching. - One client always blows up month-end

Problem: Client does bookkeeping in batches, not continuously.

Fix: Move that client to weekly reconciliation; keep discrepancies small. - Review partner keeps rejecting the same rec

Problem: Missing documentation for timing items.

Fix: Add standardized reconciliation notes with supporting evidence attached. - Cash balance ties, but nobody can explain every line

Problem: Items netting out by coincidence, not proper clearance.

Fix: Force every variance into a categorized reconciling-item list; resolve individually.

Ready to see what reconciliation looks like when the data arrives clean?

LedgerNext helps accounting firms keep client financial data clean and connected—so the numbers are right before the deadline, not after the penalty notice.

Frequently Asked Questions

How often should Canadian accounting firms reconcile bank accounts?

At minimum, monthly—but high-volume client accounts benefit from weekly or even daily reconciliation. Frequent reconciliation keeps outstanding items small, reduces month-end pressure on accounting teams, and surfaces reconciliation exceptions while supporting documentation is still easy to locate.

Why does bank reconciliation take longer for firms managing multiple clients?

Each client portfolio brings different bank formats, categorization logic, and data quality. Accounting teams must context-switch between different bookkeeping workflows, chart structures, and documentation standards. Volume scales faster than capacity when processes are manual.

Can automation fully replace manual bank reconciliation?

Automated matching handles routine transaction matching—deposits, cleared checks, standard payments. But exception items, unusual variances, and fraud flags still require human judgment. The goal isn’t eliminating manual work; it’s reserving it for decisions that actually need an accountant’s expertise.

What’s the biggest mistake firms make during reconciliation?

Treating reconciliation as the problem when the real issue is upstream: inconsistent transaction categorization, delayed client data, and fragmented bookkeeping workflows. Fixing those inputs is what actually reduces reconciliation time.