It’s 11:47 PM on a Tuesday in March. You’re staring at a screen full of unreconciled transactions across six different clients.

One bank feed disconnected three days ago and you didn’t notice.

Another client just handed you fourteen months of statements in a zip file. Your coffee went cold two hours ago.

You’re not choosing between two tools right now — you’re choosing between two fundamentally different philosophies of how accounting work should flow.

And that choice? It shapes everything downstream. Your reconciliation speed. Your error rate.

Your ability to scale past twenty clients without burning out. Let’s cut through the noise.

Quick Answer: Bank Feeds vs CSV — Who Wins?

Bank feeds are best for:

- Real-time transaction syncing with ongoing clients

- Solo bookkeeping or small client rosters

- Continuous, low-volume monitoring

CSV bank statements are best for:

- Bulk uploads and batch processing

- Historical data cleanup and backlog clearing

- Multi-client workflows at CPA firms

- Fixing messy books before CRA deadlines, T2 filings, or GST remittances

The bottom line: If you’re managing more than a handful of clients — especially during tax season — CSV-based workflows with automation give you control and scalability that bank feeds simply can’t match.

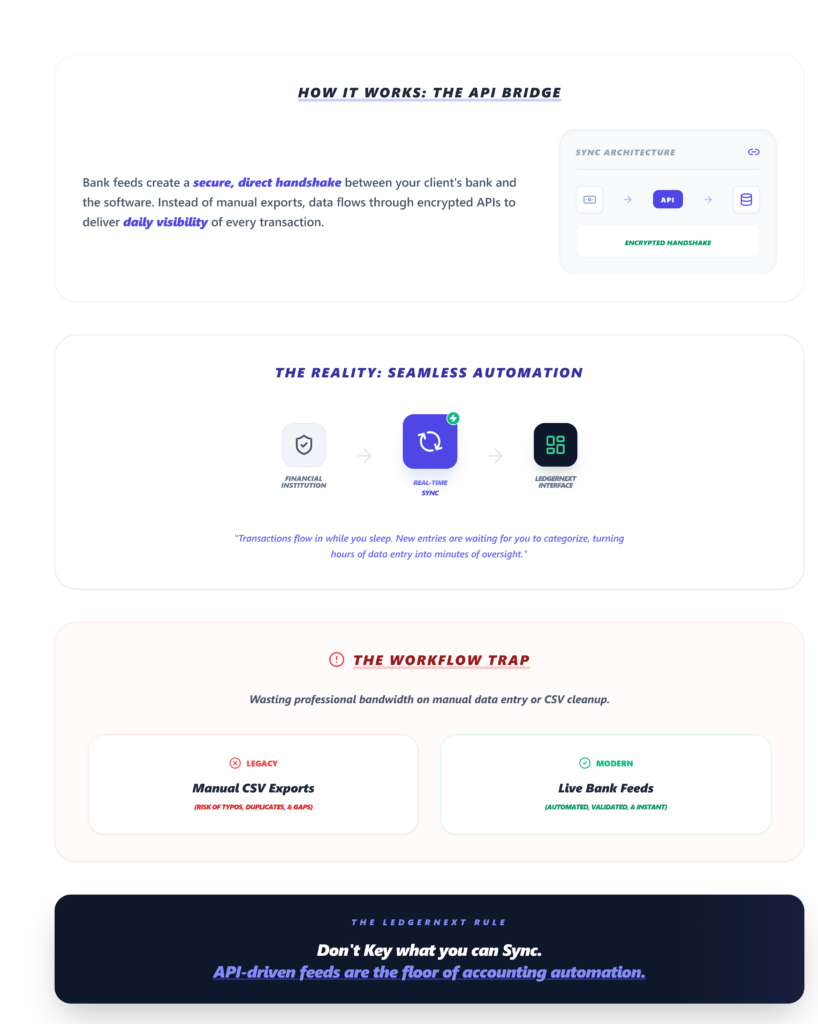

What Are Bank Feeds?

A bank feed is a direct, API-driven connection between a client’s financial institution and your accounting software.

Transactions flow in automatically — sometimes daily, sometimes in near real-time.

You open QuickBooks or Xero, and new transactions are sitting there, waiting to be categorized.

It feels seamless. When it works.

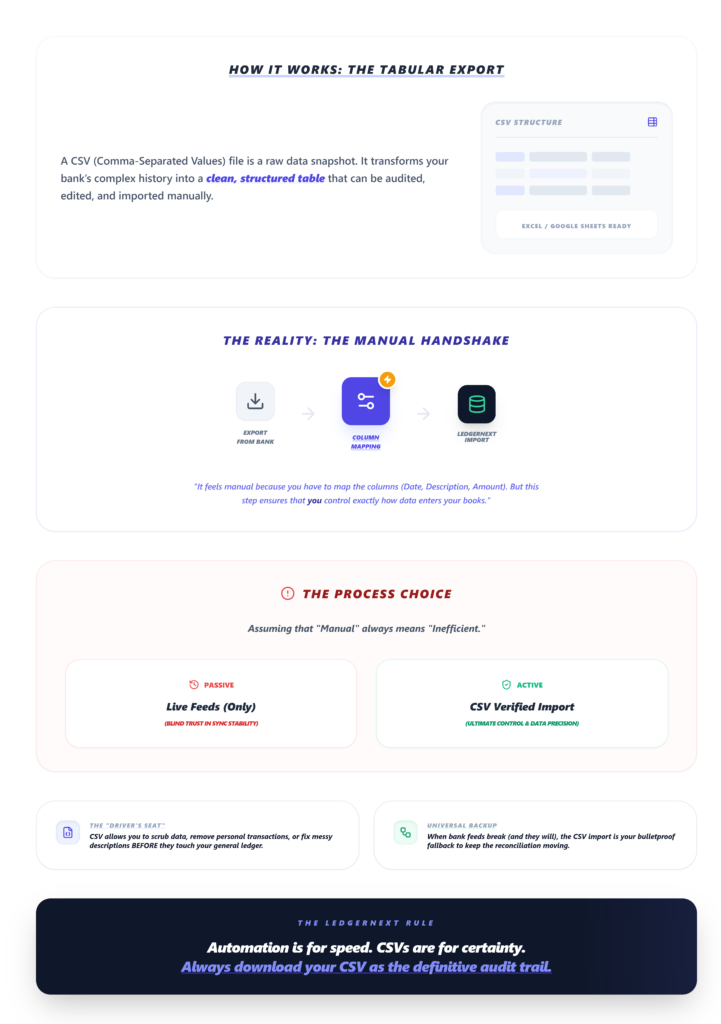

What Are CSV Bank Statements?

A CSV bank statement is a downloaded file — exported from online banking or converted from a PDF — containing transaction data in a structured, tabular format.

You upload it manually into your accounting platform, map the columns, and process the data.

It feels manual. But it puts you in the driver’s seat.

Key Differences: Bank Feeds vs CSV Statements

- Speed: Bank Feeds (Real-time or daily sync) vs CSV Statements (Batch upload)

- Control over data: Bank Feeds (Limited — what the bank sends, you get) vs CSV Statements (High — you review before import)

- Multi-client handling: Bank Feeds (Weak — each feed needs individual setup and monitoring) vs CSV Statements (Strong — bulk processing across clients)

- Historical data access: Bank Feeds (Often limited to 90 days) vs CSV Statements (Excellent — upload years of data)

- Reliability: Bank Feeds (Depends on API connection stability) vs CSV Statements (Stable — file-based, no dependencies)

- Error visibility: Bank Feeds (Errors can go unnoticed for days) vs CSV Statements (Errors caught during review/upload)

- Scalability: Bank Feeds (Degrades with volume) vs CSV Statements (Scales with proper tooling)

That table tells a story most accountants already feel in their gut. Bank feeds are convenient until they aren’t.

CSV workflows demand more upfront effort but reward you with predictability.

When Bank Feeds Work Best

Let’s give bank feeds their due. They genuinely shine in specific scenarios:

Ongoing, low-volume bookkeeping. If you’ve got a client with one business chequing account and a credit card, and you’re reconciling monthly, a bank feed is elegant.

Transactions trickle in. You categorize as you go. The matching engine in Xero or QuickBooks flags duplicates. It’s smooth.

Real-time cash flow monitoring. For clients who want to see their financial position today — not last week — live feeds deliver.

A restaurant owner checking daily deposits against POS reports, for instance.

Small client rosters. When you’re managing five or six clients, monitoring each feed connection is manageable.

You’ll notice when one drops. You’ll catch the gaps.

The friction point: You’re clicking into each client file individually, babysitting connections, re-authenticating when banks update their security protocols.

That progress bar spinning while Yodlee tries to reconnect? You’ll see it more than you’d like.

Mini-scenario: Sarah manages bookkeeping for four small businesses. She opens each QBO file every Monday, reviews the auto-imported transactions, and reconciles in under an hour per client.

Bank feeds save her real time here.

When CSV Bank Statements Work Better

Here’s where the conversation shifts — and where most scaling firms land.

Cleaning backlog data. A new client walks in with eighteen months of unfiled books. Bank feeds won’t help you.

They don’t reach back that far, and even if they did, you’d be drowning in uncategorized noise.

CSV files let you import specific date ranges, apply categorization rules, and work methodically through the mess.

This is the reality of cleaning messy data that most firms face during onboarding.

Handling multiple clients simultaneously. When you’re processing bank data for thirty, fifty, or a hundred clients — especially during T2 season — the bank feed model collapses.

You can’t individually monitor fifty live connections. CSV workflows let you batch-process.

Download statements, upload in bulk, apply rules, review exceptions. It’s a production line, not a babysitting operation.

Bulk processing for tax filing. CRA doesn’t care whether your data came from a live feed or a CSV.

They care that the numbers are right, the GST is calculated correctly, and the filing is on time.

CSV-based workflows give you the control to verify data before it hits the ledger — a critical advantage when you’re managing multiple clients under deadline pressure.

Fixing messy books. This is the big one. Bank feeds are designed for going forward.

They’re terrible at going backward. When a client’s books are a disaster — miscategorized transactions, duplicate imports, missing months — you need to rip out the bad data and rebuild from source documents.

CSV is that source document.

Mini-scenario: Dev runs a CPA firm with 60 clients. During tax season, his team downloads statements in bulk, uploads them into their processing platform, and applies standardized categorization rules across all files.

They process more in a day than a feed-dependent firm handles in a week.

The friction point with CSV: Column mapping. Every bank exports slightly different headers.

“Date” vs “Transaction Date” vs “Posted Date.” You’ll spend a few minutes per file getting the mapping right — unless your platform handles this automatically.

Why Bank Feeds Alone Aren’t Enough for CPA Firms

This is the section most comparison articles skip. They present bank feeds and CSV as equal alternatives.

They’re not — at least not for firms trying to grow.

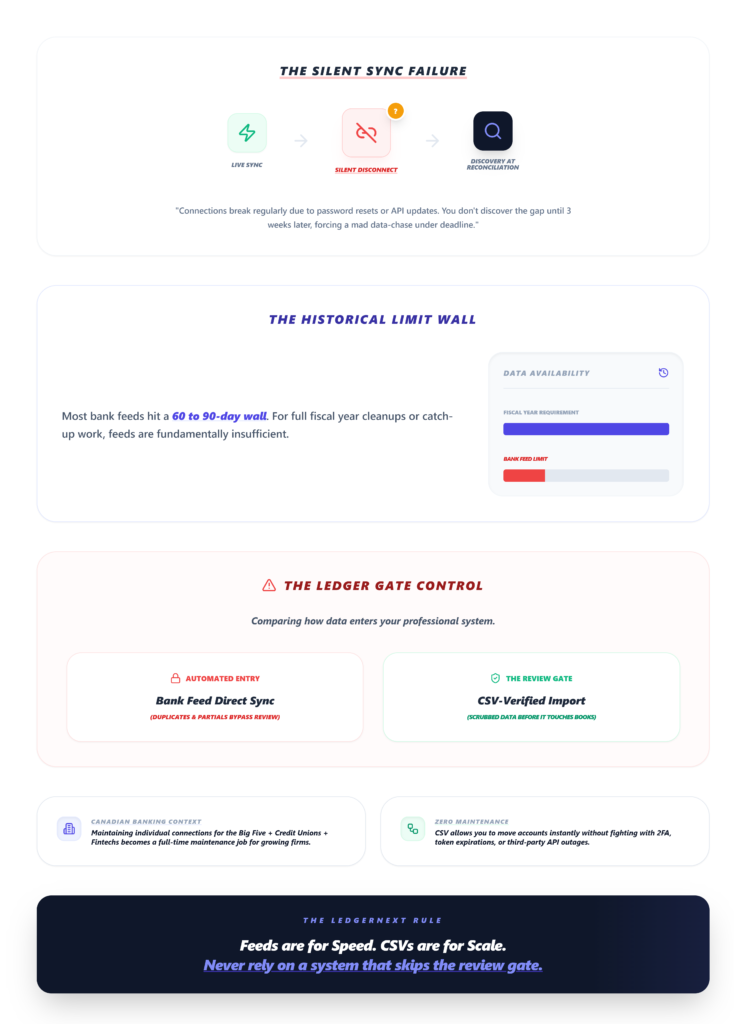

Sync failures are constant and silent. Bank connections break. Regularly. A bank updates its authentication flow.

A client changes their password. The API provider (Plaid, Yodlee, MX) has an outage.

When a feed disconnects, transactions stop flowing — but nothing alerts you loudly enough.

You discover the gap three weeks later during reconciliation. Now you’re chasing missing data under deadline.

Historical data is severely limited. Most bank feeds pull 60 to 90 days of history. Some pull less.

If a client comes to you in November needing their full fiscal year cleaned up, the feed gives you maybe September forward.

The rest? You’re downloading statements anyway.

It doesn’t scale. Setting up and maintaining individual bank connections for each client account — across multiple institutions, with varying API reliability — becomes a full-time job as your roster grows.

Canadian accounting firms dealing with the Big Five banks plus credit unions plus fintech accounts know this pain intimately.

Each connection is another potential failure point.

You lose control over what enters the ledger. With bank feeds, transactions land in your accounting file automatically.

If the feed pulls in duplicates, partial transactions, or data from the wrong date range, it’s already in your system.

Cleaning it out is harder than preventing it. CSV imports give you a review gate — you see the data before it touches the books.

How Modern Firms Actually Handle This

The firms that have figured this out — the ones processing hundreds of clients without drowning — have built a workflow that looks like this:

- Collect bank statements from clients (CSV exports or PDF conversions)

- Upload in bulk into a processing platform

- Apply categorization rules — standardized across clients or customized per engagement

- Review exceptions — the 5-10% of transactions that need human judgment

- Export tax-ready data into QuickBooks, Xero, or directly into working papers

This workflow treats bank data as raw material to be processed, not as a live stream to be monitored.

It’s a fundamentally different operating model — and it’s how firms scale past the ceiling that bank feed dependency creates.

Modern platforms like LedgerNext are built to support this exact workflow, allowing accountants to process large volumes of bank data efficiently — with automated categorization and structured outputs — without relying solely on live bank feeds.

Comparison Summary

- Bank feeds = convenience for small, ongoing engagements

- CSV workflows = control, scalability, and reliability for growing firms

- Bank feeds + CSV = the hybrid approach many firms use (feeds for active clients, CSV for onboarding, cleanup, and historical work)

CSV bank statements allow accountants to process large volumes of transactions across multiple clients more efficiently than bank feeds.

For Canadian firms handling CRA compliance, year-end filings, and multi-entity engagements, this isn’t a minor advantage — it’s operational infrastructure.

Frequently Asked Questions

Which is better for accountants: bank feeds or CSV?

For firms managing more than ten clients, CSV-based workflows with automation consistently outperform bank feeds in speed, reliability, and scalability. Bank feeds work well for ongoing single-client bookkeeping, but they introduce connection fragility and limited historical access that creates bottlenecks during busy season. Most established firms use both — but lean heavily on CSV for production work.

When should you use CSV vs bank feeds?

Use CSV when onboarding new clients, cleaning up historical data, processing bulk transactions during tax season, or working with clients whose banks have unreliable feed connections. Use bank feeds for ongoing monthly bookkeeping with stable, low-volume clients where real-time visibility matters. If you’re comparing accounting software options, check how each platform handles CSV imports — it reveals a lot about their workflow assumptions.

Do bank feeds work with all Canadian banks?

Not reliably. While major institutions generally support feeds through aggregators, connection stability varies significantly. Credit unions, newer fintech accounts, and even some Big Five bank account types experience frequent disconnections. This is why firms handling diverse client bases can’t depend exclusively on feeds for year-end accounting workflows.

Can you use both bank feeds and CSV together?

Absolutely — and most sophisticated firms do. They use feeds for day-to-day transaction monitoring on active clients and switch to CSV imports for historical cleanup, onboarding, and high-volume processing. The key is having a platform and workflow that supports both without forcing you into one model.

The Verdict

Bank feeds are a convenience feature. CSV workflows are production infrastructure.

If you’re a solo bookkeeper with a handful of steady clients, bank feeds will serve you well. But if you’re running a firm — especially a Canadian CPA practice dealing with T2 deadlines, GST reconciliation, and the beautiful chaos of tax season — your growth depends on mastering CSV-based workflows with smart automation layered on top.

Efficiency scales. Convenience doesn’t.

Ready to see how automation fits your workflow?

LedgerNext converts messy bank statements into tax-ready financial data for Canadian accounting firms.